FINTECH'S HISTORY AND PLACE IN THE TURKISH BANKING SECTOR

We tried to explain the concepts of FinTech and Islamic FinTech in our previous article. This week, we will focus on the ecosystem, historical development of FinTech, and its place in the Turkish Banking sector upon the request of our readers before going into further detail about Islamic FinTech. We cannot give an exact time when financial technologies entered into our lives. However, we can divide the history of FinTech into 3 stages with a chronological classification. We study the integration of financial products and services with technology in three stages: FinTech 1.0, FinTech 2.0, and FinTech 3.0.

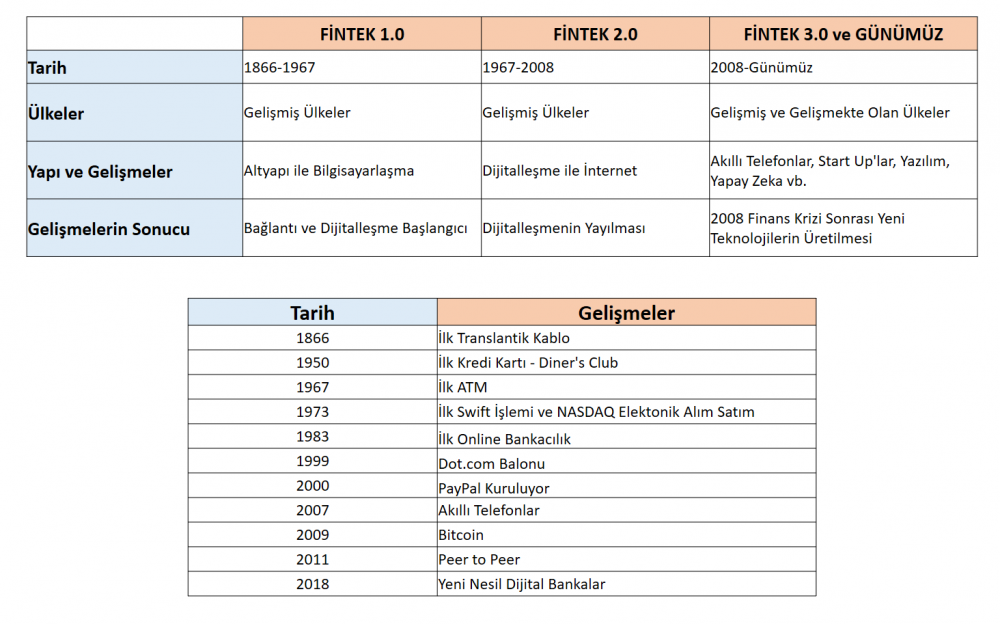

FinTech 1.0

The early period in which manual applications were used in finance and the transition to digital applications started, covers the years of 1866-1967 in the literature. The establishment of communication and technology infrastructure, and the rapid spread of payment systems after World War I stand out as the most important developments of the period.

FinTech 2.0

When we come to the period between 1967-2008, we see that the digitalisation in technologies used in communications and business transactions since 1967 led to the digitalisation in products and services offered in the financial services as well. Especially, the introduction of Internet Banking applications, credit cards, and ATMs to the sector stands out as the most significant developments of this period. The emergence of credit cards and ATMs particularly reveals the relationship between finance and technology. This development was the first step for the digitalisation of the financial services sector.

FinTech 3.0

And we come to the third period as of 2008; the most important development in this period affecting the FinTechs is the Global Economic Crisis of 2008. Financial technologies especially shine in this period with the opportunities they have provided in reducing costs, providing more transparency, and access to the intermediaries and, most importantly, financial information in the sector. Certain entrepreneurs seized the opportunity in the sector by bringing financial services and technology together, and they entered the sector with lower costs and prices. Financial technologies took shape and developed around the crises and grew substantially within the last 10 years. More effective use of information with the development of technology also led to the emergence of many innovative financial products in the last 10 years.

FinTech Ecosystem

Widely used in the field of FinTech, the term ecosystem focuses on the management style within, just like how it is used in biology. The ecosystem in biology refers to the environment and management system in which living organisms survive, and the mutual relations and the natural environment between the systems and players that preserve this continuity. The structure in this system sustains various balances and operates through mutual close interactions. And the smallest inconvenience arising in this ecosystem will affect the entire system. Now, we can apply the same definition to the structure of the financial ecosystem. We can take businesses as living organisms, and the environments of businesses create a certain order as an ecosystem. What we aim to achieve here in this section is to provide a technical explanation of the FinTech ecosystem, talk about the structure of the ecosystem, what it needs to survive, and the players of the sector.

And now, let us take a look at the shareholders of the ecosystem:

• States and their applicable policies,

• Regulatory and supervisory agencies and their applicable regulations,

• Financial structures and institutions

• Angel investors

• Consumers (Users)

• Entrepreneurs (Technology companies)

• New technological developments and infrastructure investments

• Qualified, skilled, experienced, and expert labour force

• Universities and NGOs

• Business Incubators

• Clubs, associations, and institutions that are conducting organisational activities.

Three of the shareholders above are the building blocks and main players of the FinTech ecosystem: States, financial institutions, and financial technology entrepreneurs.

FinTech in the Turkish Banking Sector

Financial technologies continue to grow rapidly around the world and in our country. Unusual developments in technology, quality, and diversity of the financial services offered, and changing customer needs have led to the formation of the FinTech ecosystem. This new dimension attracted the attention of our institutions right away, showing them the importance of FinTechs in the financial world. The FinTech ecosystem started to develop in our country especially after 2015. Enterprises, new business models, corporate collaborations, incubators and training centres, and investments are all aspects of the FinTech ecosystem in our country. Our geographical and cyclical location, successful banking and financial infrastructure, young and expert population, and dynamic entrepreneurial network all prove that we are ready to proceed in the FinTech area. The breakthroughs made between the 2017 and 2020 period especially have created an ideal environment for FinTech initiatives. Our country wishes to achieve an ecosystem with world-famous FinTech companies by carrying these steps further and attracting the attention of investors. Financial institutions have initiated their incubator and entrepreneurship centres to achieve this goal. We will talk about them and FinTech products later in our next articles. See you in two weeks, stay safe.

Burak Aktürk

Evaluate the 33h Issue of Katılım Finans!