A role model performance by Turkish participation banks for SME financing

SMEs play a major role in most economies, particularly in developing countries. They account for the majority of businesses worldwide and are significant contributors to job creation and global economic development. According to World Bank statistics, they represent about 90% of businesses and more than 50% of employment worldwide.

In addition, 600 million jobs will be needed by 2030 to absorb the growing global workforce, which makes SME development a high priority for many governments around the world. However, access to financing remains one of the most significant constraints to the survival, growth and productivity of SMEs. SMEs employ around three quarters of Turkey’s workforce and generate more than half of the economy’s total value added.

Turkey continues to implement various corporate support schemes, mostly targeting SMEs. According to the European Commission report for Turkey, in a swift response to the COVID-19 pandemic, Turkey in March set up the Economic Stability Shield package worth TRY100 billion (US$14.11 billion; 2.2% of GDP). A quarter of this support goes to doubling the Credit Guarantee Fund's limit to TRY50 billion (US$7.06 billion) to provide SMEs and companies with liquidity needs. The scope of SME support was extended to the services sector, craftsmen and artisans.

Participation banks in Turkey have also provided significant support for the continuity of economic activities as an immediate response to the pandemic. They actively put forward their digital products and services to customers, postponed installments of specific payments and applied flexible limit allocation for increasing financing volume to both retail, SME and corporate customers.

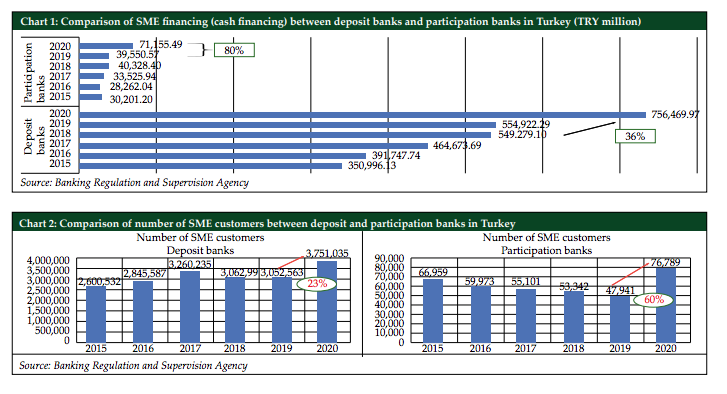

In Chart 1, the total volume of SME financings increased at both deposit and participation banks during the period of 2015 to 2020. However, participation banks’ performance level saw a substantial increase at 80% during 2020 compared to the performance level of deposit banks at 36%. In Chart 2, the number of SME customers increased at both deposit and participation banks during the period of 2015 to 2020. However, the number of SME customers of participation banks reached 76,789 with an outstanding increase at 60% during 2020 compared to the increase of deposit banks at 23%. The COVID-19 pandemic is affecting

the economy and SMEs in several ways. Among the many challenges, liquidity constraints represent a crucial concern for many firms, especially smaller ones. A recent survey in China, for example, highlights that one-third of surveyed SMEs only had enough cash reserves to cover fixed expenses of one month and another third for two months. Policymakers around the globe are taking action to prevent viable firms from going bankrupt because of temporary liquidity shortages.

In addition to an agile response to the COVID-19 pandemic from the Turkish government, participation banks have given a role model performance for both OIC countries and also other jurisdictions in which SMEs are suffering severely from the impact of COVID-19. Fatma Cinar is the head of international relations at the Participation Banks Association of Turkey. She can be contacted at [email protected].

Source: IFN

Evaluate the 33h Issue of Katılım Finans!