Utilized as the driving force of the development, the concept of innovation may be described as the transformation of the information into economic value in the briefest sense. Looking at the service channels and historical development of the innovations happening in the banks, we see that what led to the open banking concept of today was the ATM and telephone banking between 1970-1980, internet banking in the 1990s, the establishment of the foundation of the digitalization journey through mobile banking in 2000s, and appearance of Fintechs following the crisis of 2008. The fundamental reason for the formation of all this digitalization cycle may be expressed as the elimination of the need for customers to physically go to the banks and the active role this convenience has played in the innovative undertakings to serve humanity.

In particular, the fact that Fintechs;

• Employ a perception of technology that is different than traditional approaches,

• Utilize technology in a different way,

• Focus on single or multiple topics,

• Specialize in these topics and quickly meet the customer expectations,

In spite of these, the fact that banks;

• Are large and strong organizations,

• Possess a broad customer base,

• Have great experience,

• Own a reliable and potent capital structure,

have forced the Fintechs and the banks to establish cooperation and the "open banking" concept has begun to make its way into our lives more and more and become an intensively addressed topic.

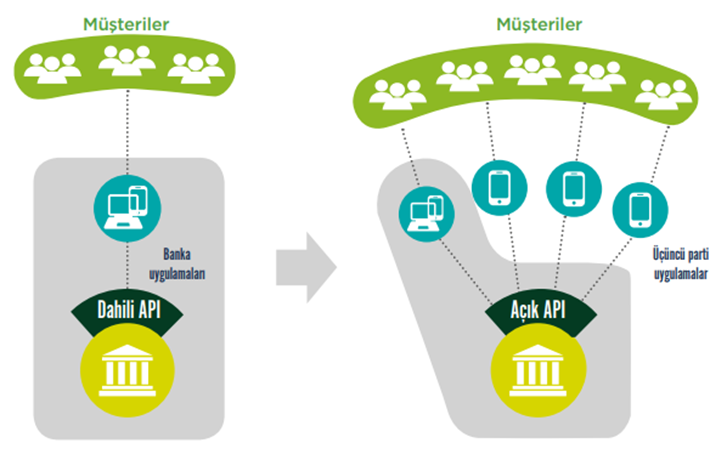

As I tell about the developments and innovations in the banking sector, I would like to mention how the existing structure is perceived in terms of customer expectation and compatibility. It seems like while the fact that people are able to adapt to the convenience of the technical transactions leads to positive consequences, this may also bring certain difficulties. The issue of trust and adaptation to the new procedure ranks at the top of this list. Because the change in the existing order is not considered acceptable right away as it will cause uncertainty for people. Hence, such connections formed between the customers and banks should be detected and the problems should be minimized. At this juncture, we may consider the open banking concept brought to us by the open innovation concept a solution. Open banking is a concept where customers can easily manage their financial assets, track them on a single platform, and make the most appropriate choice by evaluating all the opportunities at the same time. The difference in process between traditional banking and open banking is shown schematically in Figure 1:

Figure 1. Traditional Banking and Open Banking

Source: Fintech Istanbul 2019, Open Banking around the World and in Türkiye: The Future of Banking

As shown in Figure 1, when bank customers work with more than one bank, they can also perform their transactions with third-party applications with the concept of open banking. While this was an initiative undertaken by banks at first, it spread over time and became an approach accepted worldwide and required by law. (Fintech Istanbul, 2019)

To put it simply, Open Banking is a process of making the data of customers in the financial system accessible to authorized "Third Party Providers" (TPP) through Application Programming Interfaces (API) in compliance with the regulations.

Participation Banks and Open Banking

It seems that we can tell that the digitalization process has accelerated recently for participation banks based on interest-free banking principles. With the driving force of the Covid-19 pandemic, the number of active digital customers which was 3.1 million by the end of the 3rd quarter of 2020 reached 3.6 million by the end of the third quarter of 2021, according to the statistics of the Participation Banks Association of Türkiye. (TKBB, Research Report, 2021) This has brought concepts such as improved customer experience, new generation technologies, digitalization, access to financial opportunities, fintech ecosystem, and open banking within participation banks. The development of these concepts encouraged participation banks to remain competitive in the market and improved them.

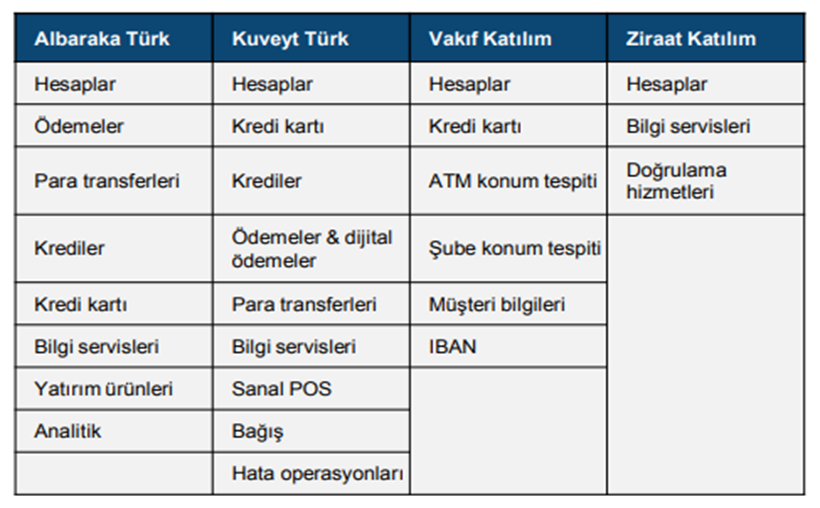

We can tell that an open banking experience in participation banks is a significant step in ensuring transparency and economic justice. Because open banking offers open data circulation in the participation finance sector. In this context, the circle of trust is built between the parties in a healthy manner. Figure 2 depicts the API transactions offered by certain participation banks serving in Türkiye.

Figure 2. API Transactions Offered by Four Participation Banks Serving in Türkiye

Source: TKBB, Participation Banking Digital Research Report, 2021

The state shown in the table may be interpreted as that participation banks have caught the world trend. The fact that open banking represents an opportunity within the financial sector also points out to the necessity of this adaptation. Because the concept of open banking is a sign of a transformation in the traditional banking system. It is also critical for participation banks, as it is for traditional banks, to develop in parallel with this trend in terms of creating their own ecosystem. In particular, it will enable participation banks to focus more on open banking, deliver their products and services to more customers as a result of the increasingly competitive environment, reduce their costs, be fast and easily accessible, offer alternative products to their customers along with a smooth experience, increase customer loyalty, and deepen their customer pools.

Many reports, blog posts, and articles have been written about open banking. Our aim in this article was to explain how open banking emerged and to give a brief description of participation banks through a simple definition. Our readers, who are interested in obtaining further information in this regard, can reach it by searching, as well as waiting for our future articles. Hope to see you in our future articles...

Burak AKTÜRK – Zeynep ŞAKARCAN

Evaluate the 33h Issue of Katılım Finans!