Elements Distinguishes Murabahah from Interest-bearing Financial Methods

The most prominent one among the financing methods applied by the Participation Banks is the method of sale with a profit statement. This financing method is called 'Murabahah' in the literature, yet commonly referred to as 'Corporate Financing Support' and 'Retail Financing Support' in corporate and customer relations. The share of murabahah transactions among the total activities of banks operating not only in Turkey but also around the world and offering products and services within the framework of principles of Islam is estimated to be 80% or more.

Murabahah as a Financing Method

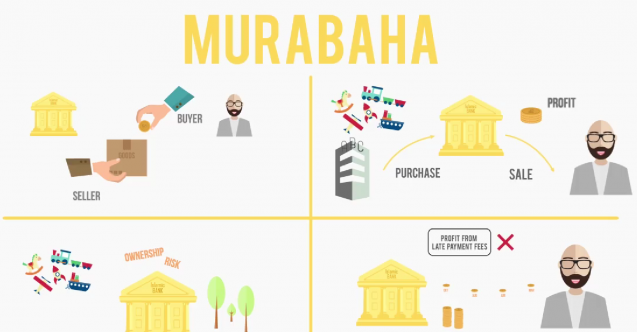

Murabahah transactions are performed through the purchase of a commodity by the Participation Bank under the customer's instruction and promise of purchase by adding a certain profit on the price or cost of the commodity and selling it to the buyer, who is the customer, on a deferred basis. Since the rate of return is fixed in Murabahah transactions, it is not considered as a financial method based on profit-loss sharing. Meeting the needs of customers is also important under this method.

4 Key Characteristics Differentiating Murabahah from Interest-bearing Financial Methods

The fact that the rate of return is predetermined causes the relevant financial methods to be confused with the interest-bearing financial methods. However, in case we look at this issue in terms of the Sharia, there are 4 main features that distinguish the murabahah method from interest-bearing financial instruments:

1. Transactions are performed over the commodities and services subject to sale instead of direct borrowing or lending transactions. (As we have experienced in the past months, converting the TRY loans received into foreign currency and attempting to earn revenue from the exchange rate difference is prevented.)

2. Suggesting two different price offers for the cash or deferred sale of a commodity has been deemed legitimate by Islamic jurists. The person who buys commodities on a deferred basis will have what s/he needs in advance and spread his/her debt over time. The seller, on the other hand, regards deferred sales as a marketing method and thus aims to make a profit. (Late charge is found in the money-commodity exchange where there is no currency unity and interest is found in the transactions where there is a currency type unity between the prices.)

3. In terms of principles of Sharia, a person cannot sell or rent a commodity that s/he does not own. Therefore, financial institutions undertake the risks that may arise when they take ownership of the commodities subject to sale.

4. Finally, it is the price that is stipulated and agreed upon in the sales contracts, not the interest. Therefore, in case payments are delayed due to unexpected circumstances, no change should be made in price. (In order to prevent abuses, a delay penalty may be applied in such cases. However, Participation Banks cannot benefit from the portion of the amount they receive as a delay penalty, above the costs they have incurred for the collection of the receivables and the inflation rate.)

Aspects Open for Improvement

In addition to focusing on credit spreads in Murabahah transactions, there are various actions that can be taken by both financial institutions and relevant legal authorities, such as encouraging commercial activities and supporting it along with various sector researches, receiving of the commodities by the financial institution and undertaking responsibility for damage in a way that does not cause grievances. Even though there are various aspects that are open for improvement, the views that murabahah is similar to the same interest-bearing financial methods are generally not dependent on proper research and do not offer alternative solutions.

Having contributed a lot to the field of Islamic economics and finance through his research and studies, Mohammed Umer Chapra, a Pakistani economist, emphasizes that what marginalizes the Islamic financial system is not the lack of a large number of products, but the failure to reflect the solid foundations and logic behind the transactions to the society. The most significant basis for the acceptance of solid foundations by society depends on the fact that they can be applied in the most correct manner by the Participation Banks.

Eyyüp Yakup Gedikli

Evaluate the 33h Issue of Katılım Finans!